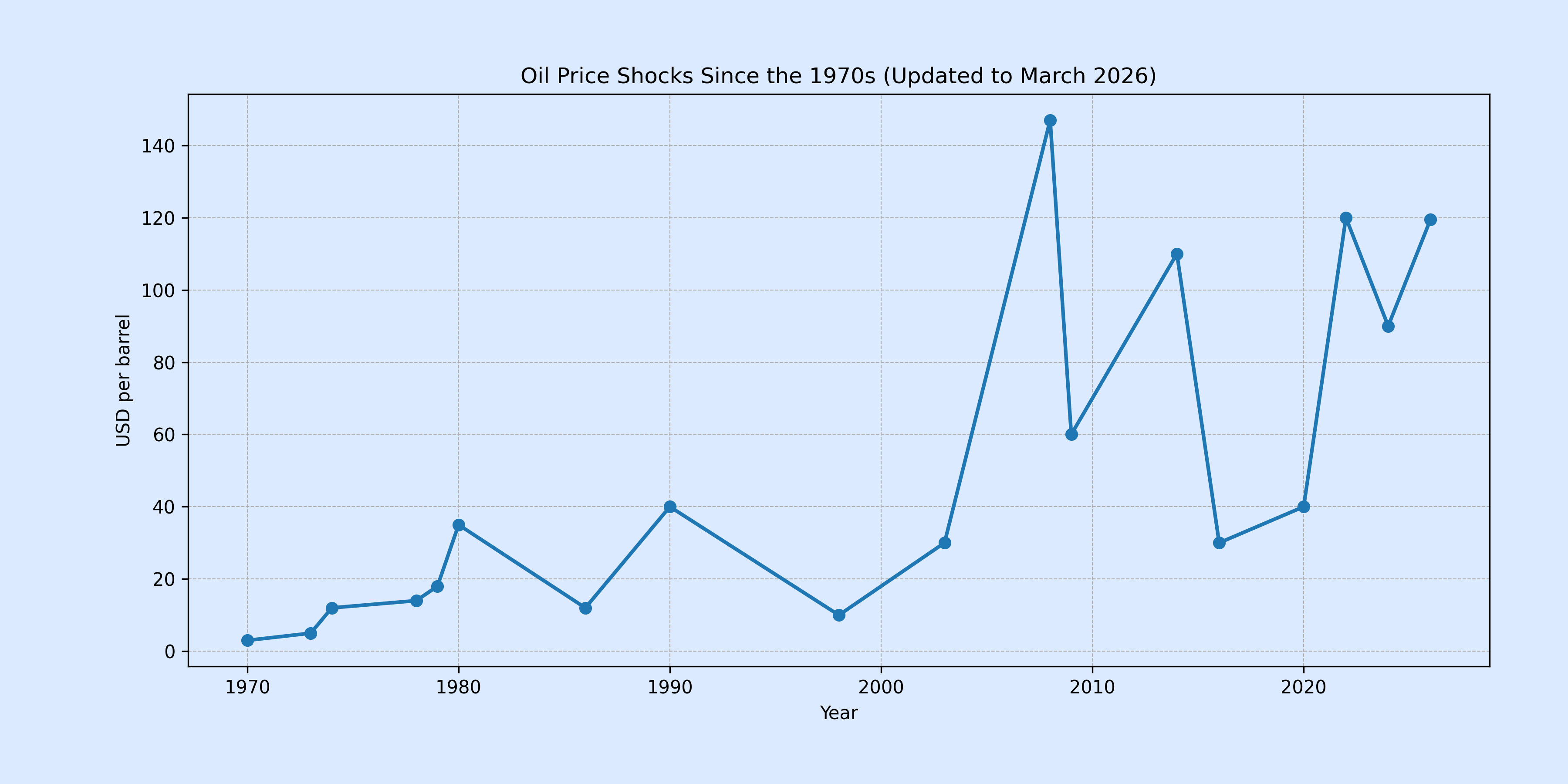

Oil price shocks are often described as rare geopolitical events. Over the past half-century there have been only a handful of truly systemic ones: 1973 (the OPEC embargo), 1979 (the Iranian Revolution), 1990 (the Gulf War), 2008 (the commodities supercycle), 2022 (Russia’s invasion of Ukraine) and, possibly now, the conflict between the United States and Israel against Iran.

In practice, these episodes produce something far more concrete: large redistributions of wealth. When Brent crude swings violently within hours, billions of dollars change hands in financial markets long before the real economy has time to react.

The dynamic can already be seen in Brazil’s stock market. Since January 2, 2026 — the eve of the kidnapping of Venezuelan president Nicolás Maduro — shares of Petrobras have risen nearly 40%. Over that period, the company’s market value jumped from roughly R$400bn to about R$563bn, creating close to R$160bn in market wealth in just over two months.

The company itself, however, remains essentially unchanged. The oil fields are the same, the platforms are the same and the barrels beneath Brazil’s pre-salt reserves have not moved. What changed was the expected price of oil — and with it the speed at which markets redistribute wealth.

In the real economy, the effect moves more slowly — but it is already visible. Between the Strait of Hormuz and Brazil’s gasoline pumps runs a long transmission belt passing through traders, fuel distributors, petrochemicals, fertilisers and road freight.

Fuel distributors have already begun adjusting prices, and gas station owners report daily increases of R$0.02 to R$0.07 per litre. In industry, petrochemical producers such as Braskem face rising naphtha costs, with resin price adjustments that can reach R$2,000 per tonne. Agriculture also feels the shock: Brazil imports about 85% of the fertilisers it consumes.

More expensive diesel then ripples through Brazil’s road-based logistics system. Freight rates rise, distribution costs increase and sectors heavily dependent on transport begin recalculating margins. Consumers, sooner or later, end up receiving the increase.

Once this transmission reaches final prices, it begins to appear in inflation data — and inevitably enters the radar of the Central Bank.

Unlike the early oil shocks, Brazil has built a more resilient economy over the past two decades and has become a net exporter of crude oil, largely thanks to the development of its pre-salt reserves. Yet vulnerabilities remain. Dependence on imported fertilisers, exposure to diesel imports, and the absence of certain strategic industrial supply chains still leave the economy sensitive to swings in the barrel.

If oil continues to be a recurring source of global turbulence, Brazil’s challenge will be to turn its status as an energy exporter into an industrial strategy capable of reducing those vulnerabilities.

If the recent surge in the barrel persists, the debate will no longer be simply about the price of oil.

It will be about who captures the gains — and who absorbs the costs.

Leave a Reply