TerraBras — the proposed state-owned company designed to manage Brazil’s rare earth wealth — appears to have died before it was even born. That may be the best possible test for Brazil’s critical minerals policy: separating the right question from the wrong answer. The right question is how Brazil can avoid becoming a cheap exporter of strategic minerals. The wrong answer would be creating a state mining company and expecting it to solve, by decree, a value chain that depends on technology, capital, chemical processing and industrial buyers.

The Brazilian government has already signaled that it does not want a new public company for critical minerals. Development Minister Márcio Elias Rosa has said he sees no need for a state-owned company in the sector, while the economic team supports regulation, sovereignty and value added — but without large fiscal incentives. The declared priority is different: ensuring that critical minerals are processed in Brazil rather than exported as raw material. That is the right agenda. The question is how to make it work.

The political death of TerraBras does not kill the debate over production sharing in mining, which was part of the same discussion. Quite the opposite. It allows Brazil to discuss the instrument without the burden of a new state apparatus. In mining, production sharing can make sense only if it is understood not as nationalization of production, but as a sovereignty clause over scarce, geopolitical and hard-to-replace resources.

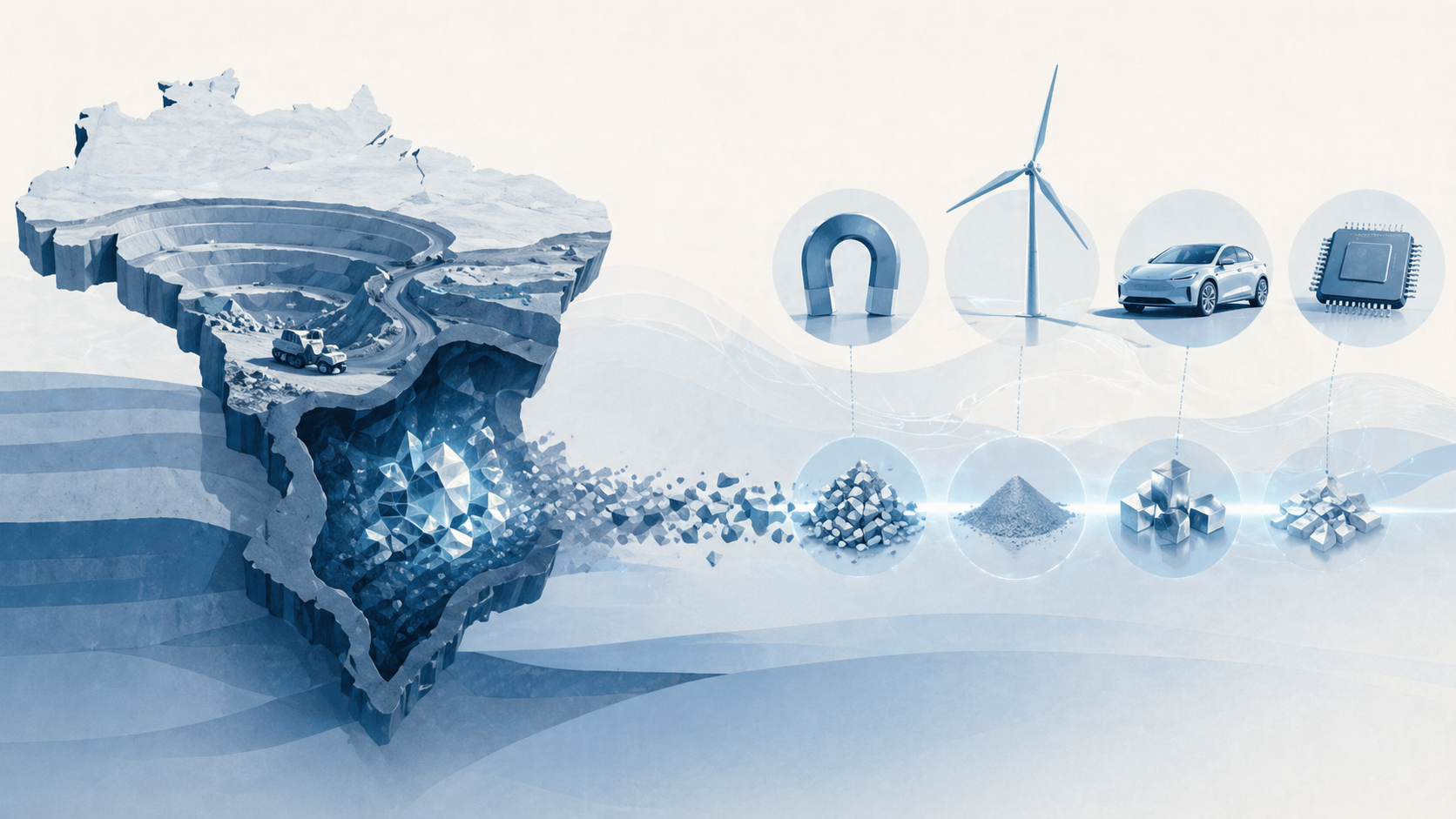

Rare earths are not ordinary minerals. They are used in permanent magnets, electric vehicles, wind turbines, military equipment, electronics and energy transition technologies. China dominates a large part of global processing. The United States, Europe and Asia are looking for alternative suppliers. In this context, Brazil has bargaining power. But bargaining power is not the same as industrial capacity. Having the resource underground does not mean mastering separation, refining, alloys, magnets or long-term industrial contracts.

That is where the comparison with Brazil’s pre-salt oil fields becomes misleading. Oil could support a production-sharing regime because there was scale, Petrobras, giant reserves, predictable demand, accumulated technology and an existing supply chain. Rare earths are different. Geological risk may be lower in some projects, but technological, chemical and commercial risks remain high. Separating and refining oxides requires know-how. Turning them into industrial inputs requires buyers, standards, certification and investment. A rule that is too heavy could scare away precisely the capital Brazil needs to attract.

A pure production-sharing model, in this case, would be a mistake. It could become another Brazilian regulatory oddity: attractive in nationalist speeches, but damaging for investment. Junior miners, specialized funds and technology companies do not enter high-risk projects if, before the first industrial plant is built, they already have to share physical output with the state, negotiate complex contracts and live with political uncertainty. Brazil needs to capture value without frightening the value chain before it even exists.

But rejecting any form of additional value capture would also be naive. Brazil should not repeat the old model of opening the mine, exporting concentrate and importing finished technology. Value is not captured only at the extraction stage. If Brazil accepts only traditional royalties, it risks selling the raw material of the energy transition and buying back the technology at a premium.

The smarter path would be selective sharing. Not a monopolistic TerraBras. Not a state company pretending to be a shortcut to industrial policy. Instead, Brazil could create a regime in which the federal government demands additional commitments from strategic projects: local processing, upside participation, technological content, priority supply for domestic value chains and research and development obligations.

That does not necessarily mean mandatory physical production sharing. Brazil could use variable royalties, price-linked bonuses, minority participation through BNDES or public funds, golden shares in sensitive assets and gradual industrialization targets. The state does not need to operate the mine to capture part of the strategic rent. It needs to design better contracts.

The real choice is not between nationalization and laissez-faire. It is between exporting geological wealth and building industrial leverage. In critical mining, sovereignty does not mean owning a state company. It means making private investors understand that, to take the mineral out, they must leave part of the value chain behind.

Leave a Reply